Commercial

enterprises are driven by profit motive – that is entirely normal and to be

expected. Other motives might be secondary – educating customers, improving

health or addressing social issues, but the need for profit is always the

driving force. I have no problems with that. However...

|

| 'Financial Inclusion' means big profits for the banks |

Wanting it ALL

In

the case of banks, we are now faced with a situation that financial

institutions are grabbing too much power and influence over our lives in their

drive to make as much money as they can. What they call 'inclusion' is in reality a system to EXCLUDE from society anyone who refuses to sell their soul to the new dictatorship. One market is not enough – they want

it ALL. The deceptively named ‘financial inclusion’ looks set to become a

system of slavery to the banks and their ‘partners’ like governments, big

pharma and ‘telcos’ or telecommunication companies.

“Mainstream banks tend to work outside the spotlight but are quietly driving financial inclusion forward.”

This is

just one of the many damning sentences I have just read in a report entitled “The Business of Financial Inclusion: Insights from Banks in Emerging Markets”.

I don’t

need to do any writing of my own in this article. I have jotted down the most

damning statements from the report below.

"Financial inclusion is widely recognised as one of the most important engines of economic development."

Oh really?

I always thought it was productivity and the economic freedom to be productive.

"Access to formal financial institutions allows poor households to expand consumption."

Or do they mean ‘living beyond their humble means’ and get into debt?

"Partnerships with telcos, fintech companies, retailers and other firms have enabled banks to broaden their array of products.By tapping into multiple information sources, including social media and credit bureaus, banks are using more sophisticated data analytic techniques to target underserved customers in a more personalized way.Despite the encouraging trends documented in this report, close to 2 billion adults around the world still lack access to an account. In order to bring the benefits of financial inclusion to them, banks will have to improve their business models, bolster customer trust, and build customer capability to use financial services. Equally important, policy makers will need to develop and implement legislation that facilitates and supports digital banking and promote financial inclusion for all."

Or: banks

calling for laws to help them increase their power and their profits. They can’t

leave those 2 billion untapped – all that money to be made off those hapless

individuals!

Phrases

like these are used extensively throughout the document:

- Business strategy, aggressive growth plans

- A few are more focused on corporate social responsibility

- Customer acquisition

- Partnerships, financial ecosystem (with governments) Banks may seek partners to help customer targeting and acquisition

Here is the

reason for the much reported drive for cashless societies:

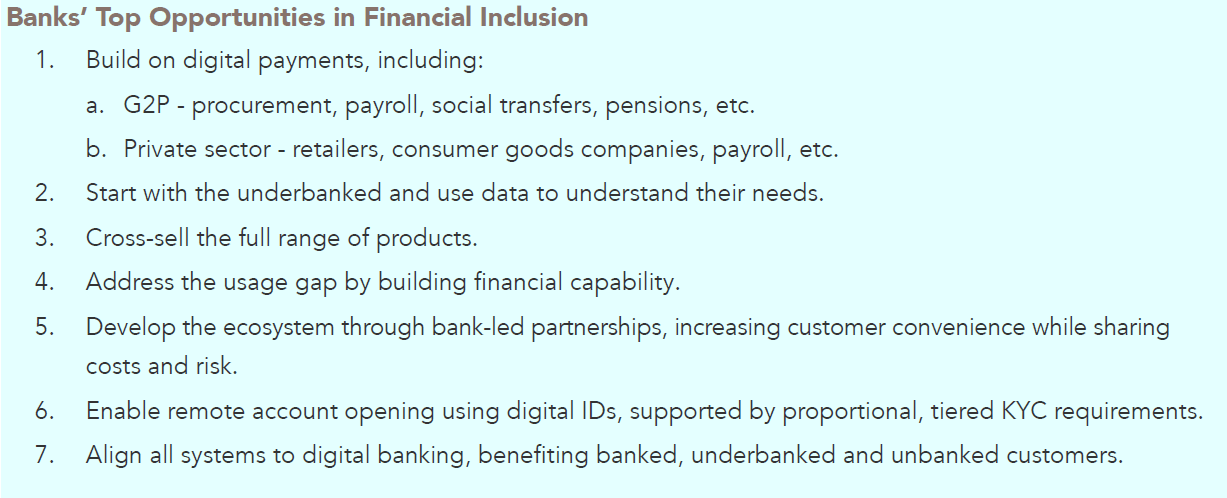

"Digital payments are the main gateway to new customers""Technology helps banks to reduce the cost of identity verification through national ID systems that increasingly rely on biometrics""Increasing merchant acceptance so digital acceptance will be more useful to customers"

Now we

understand the Visa story. But banks

have problems too.

That is why they prefer to work out of the limelight. Public awareness campaigns are a big problem for them. To quote again:"Challenges: customer trust, public awareness campaigns."

"Mainstream banks tend to work outside the spotlight but are quietly driving financial inclusion forward."

But look what they have achieved already:

"Policy makers in most countries are cooperating with banks to advance financial inclusion initiatives"

That means

governments.

"Align all systems to digital banking"

"While news headlines about financial inclusion often focus on mobile money and the entry of telco companies, the bigger story is right at the core of the financial system – with the banks. Mainstream banks tend to work outside the spotlight but are quietly driving financial inclusion forward.""The trends are dynamic; approximately 721 million adults gained access to new financial accounts between 2011 and 2014, and over 90 percent of these (666 million) opened accounts at financial institutions, with the remaining opening a mobile account as their primary account.""The increase in bank accounts is equally impressive and significant, given the banks’ already massive reach."

Arrogant.

And still it is not enough for them.

"These numbers demonstrate that banks already serve most of the world’s population, including those of lower income, and that they represent a formidable, dynamic force for expanding inclusion. Important changes are underway."

Yes. It’s

the United Nation’s ID2020 project I keep reporting about. A biosensored number

given to us at the point of vaccination, without which survival becomes nigh

impossible.

"Men have higher levels of account ownership than women by an average of 9 percentage points in developing countries. Banks identify the women’s market as underserved and profitable""The State Bank of India (SBI) is embracing Prime Minister Modi’s historic push for inclusive finance. In 2014, 90 percent of small businesses in India were reported to have no link to the formal financial sector, and only 40 percent of the population had a functional bank account. Thanks to SBI and other banks, the story has changed dramatically; 53% of the population held accounts as of 2015."

This is

astonishing. In the space of only one year, and with the help of the Indian

government, the banks added vast numbers of new customers to their portfolios.

Conclusion: in this boastful and greedy document, banks are showing their true colours. Vast profits are not enough, they want it ALL. And they work closely together with governments and other partners, but we already knew that. The most frightening thing to me is the speed with which their intended changes can overwhelm a nation, as we saw in India recently.

Conclusion: in this boastful and greedy document, banks are showing their true colours. Vast profits are not enough, they want it ALL. And they work closely together with governments and other partners, but we already knew that. The most frightening thing to me is the speed with which their intended changes can overwhelm a nation, as we saw in India recently.

There are

further major changes afoot in India,

and I hope to bring you that story as soon as possible too. ID2020 is

fast approaching, and it doesn’t look good.

No comments:

Post a Comment